IRS Payment Plan Ineligibility: Reasons & Next Steps

Confused about why you are not eligible to create a pre-assessed payment plan with the IRS? Discover the reasons and explore your next steps to handle your tax obligations effectively.

Deborah Olson

9/16/20257 min read

IRS Not Eligible for Pre-Assessed Payment Plan? Why & Your Next Steps

You logged into your IRS online account, ready to set up a payment plan for your tax debt, only to be met with a frustrating message: "Not Eligible." This immediate rejection of a pre-assessed, online payment plan can feel like hitting a wall, leaving you confused and worried about what comes next. The good news is that this is not a final verdict on your ability to resolve your tax situation. It simply means your case requires a different path than the automated, streamlined route.

The Internal Revenue Service is a vast agency, and its collection efforts are significant. In fiscal year 2024, the IRS collected $120.2 billion in unpaid assessments on returns, highlighting the importance of taxpayers proactively addressing their liabilities. This article will demystify why you might have been denied an online payment plan, explain the different types of agreements available, and provide a clear, step-by-step roadmap for your next actions.

Understanding "Pre-Assessed" vs. Other IRS Payment Plans

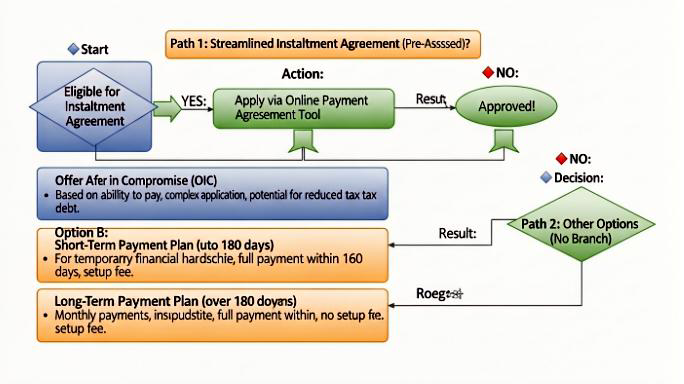

Different paths to setting up an IRS payment plan based on eligibility.

When the IRS denies an online request, it's crucial to understand what you were applying for and how it differs from other options. The denial is often for a specific type of plan, not for all possible solutions.

What is a "Pre-Assessed" or Streamlined Installment Agreement?

A "pre-assessed" or Streamlined Installment Agreement is the simplest and fastest type of IRS payment plan. It's typically handled through the Online Payment Agreements (OPA) tool available in your IRS online account. This system uses the information the IRS already has on file to make an instant decision. If your financial situation and tax debt fall within certain predetermined, low-risk thresholds, the system can approve you in minutes without requiring you to submit detailed financial documents or speak to an agent.

The Appeal and Benefits of Easy Online Payment Plans

The appeal of the online system is obvious: it’s fast, convenient, and avoids the potential stress of a phone call with the IRS. You can set up your plan from home, choose your preferred payment methods like a direct debit from a checking account, and receive immediate confirmation. This automated process is designed for straightforward cases, allowing millions of taxpayers to resolve their debts efficiently.

How All IRS Installment Agreements Work (Generally)

Regardless of how you obtain one, all IRS installment agreements share a common purpose: they allow you to pay your tax liability over time in manageable monthly payment amounts. An approved installment agreement prevents the IRS from pursuing more aggressive collection actions, such as wage garnishments or bank levies, as long as you adhere to its terms. However, it's important to remember that penalties and interest continue to accrue on your unpaid balance until it is paid in full.

Key Reasons You Might Be Denied the Streamlined Option

The automated OPA system has strict criteria. If your account has any flags that fall outside these parameters, it will automatically deny the request and direct you to a more manual process. Here are the most common reasons.

Exceeding the Maximum Tax Debt Threshold

The most frequent reason for an online denial is the total amount you owe. For individuals, the threshold for a streamlined agreement is typically $50,000 (including tax, penalties, and interest). If your total tax debt exceeds this amount, the IRS requires a more detailed financial review before approving a long-term payment plan, making you ineligible for the automated system.

Specific Tax Debts or Unfiled Tax Returns

The IRS requires taxpayers to be in full compliance before granting a payment plan. This means you must have filed all required tax returns for previous years. If you have an outstanding tax return from any recent tax year, the online system will reject your application. Furthermore, certain types of tax debt, particularly business-related liabilities like Trust Fund Recovery Penalties, often require manual review and are not eligible for the streamlined process.

History of Non-Compliance or Defaulting on Past Plans

Your payment history matters. If you have previously entered into an IRS payment plan and defaulted on it by missing payments or failing to stay current on new tax obligations, the system will flag your account. This history of non-compliance makes you a higher risk, and the IRS will require a more thorough review before granting another agreement.

Complex Account Status Requiring Detailed Financial Review

Several account statuses can trigger an automatic denial for an online plan. These include being in an active bankruptcy proceeding, having an Offer in Compromise pending, or being currently under an IRS audit or examination. In these situations, your account requires specialized handling that the automated system is not equipped to manage.

Other Administrative and Technical Barriers

Sometimes the reason is purely administrative. For instance, if you just filed your tax return and the full balance hasn't been officially assessed and posted to your account, the OPA tool may not be able to process your request. Similarly, recent payments that haven't cleared or other data discrepancies can cause temporary ineligibility.

Your Roadmap: What to Do When the Online Path Is Closed

Being denied online is not a dead end. It's a detour. Here is a clear, four-step process to follow to get back on track.

Step 1: Verify and Understand the Specific Reason for Denial

Before taking action, try to determine why you were denied. Log back into your IRS online account and carefully read any messages or notices. Check your account balance and status for each tax year. An official IRS notice sent by mail may provide a more detailed explanation. Understanding the root cause—whether it’s the debt amount, an unfiled tax return, or another issue—will guide your next steps.

Step 2: Prepare for a More Comprehensive Financial Disclosure

Since the streamlined option is off the table, you will likely need to provide the IRS with detailed information about your financial situation. Begin gathering key documents, including recent pay stubs, bank statements, monthly expense records, and information about your assets. This information is used to complete a Collection Information Statement (CIS), such as Form 433-F, which the IRS uses to determine your ability to pay.

Step 3: Proactively Engage with the IRS for a Non-Streamlined Installment Agreement

You can apply for a manual installment agreement in two primary ways: by mail using Form 9465, Installment Agreement Request, or by calling the IRS directly. For larger or more complex debts, attaching a completed Collection Information Statement with your Form 9465 can expedite the process. Be prepared for a more in-depth conversation if you call, using the financial documents you gathered in Step 2 to answer questions accurately.

Step 4: Consider Other Viable IRS Resolution Options

An installment agreement is not the only solution. Depending on your circumstances, other payment plan options or resolutions might be more suitable. These include a short-term payment plan, an Offer in Compromise, or being placed in Currently Not Collectible status. It’s wise to be aware of all possibilities as you move forward.

Exploring Non-Streamlined Installment Agreements and Alternatives in Depth

When the online door closes, several other doors open. Here’s a closer look at the primary alternatives.

Non-Streamlined Installment Agreements: The Next Tier

This is the standard long-term payment plan for those who don't qualify for the streamlined version. It requires submitting Form 9465 and, for balances over $50,000, usually a Form 433-F. The IRS will analyze your income, expenses, and assets to negotiate monthly payment amounts that you can afford and that will pay off the debt within the collection statute of limitations (generally 10 years).

Short-Term Payment Plans: For Temporary Relief

If you can pay your full tax debt within 180 days, you may qualify for a short-term payment plan. This option has a higher balance limit for online application (up to $100,000) and, crucially, does not have a setup user fee. While interest and penalties still apply, it’s a cost-effective way to get more time without committing to a formal installment agreement.

Offer in Compromise (OIC): When You Can't Pay What You Owe

An OIC allows eligible taxpayers to resolve their tax liability with the IRS for a lower amount than what they originally owed. The OIC program is intended for those experiencing significant financial hardship, and the qualification process is rigorous. The IRS will look at your ability to pay, income, expenses, and asset equity to determine if you are a viable candidate.

Currently Not Collectible (CNC): Temporary Hardship Status

If you can prove to the IRS that you are unable to pay your basic living expenses and also pay your tax debt, the agency may place your account in Currently Not Collectible status. This is not a permanent solution; it's a temporary pause on collection activity. The IRS will review your financial situation periodically, and if your income increases, they will resume collection efforts.

Partial Payment Installment Agreement (PPIA): Paying What You Can Afford

A PPIA is a specialized type of installment agreement for taxpayers who can make monthly payments but cannot pay their tax debt in full before the collection statute expires. It requires a complete financial disclosure, and the IRS must agree that you cannot pay more. It’s a complex option that often requires professional assistance to negotiate.

Critical Considerations for Any IRS Payment Arrangement

No matter which path you take, keep these key factors in mind.

Fees, Interest, and Penalties: The Ongoing Costs

Setting up a long-term installment agreement typically involves a one-time user fee. Furthermore, a payment plan does not stop the clock on interest and late-payment penalties. These charges will continue to be added to your account until the balance is zero, so paying the debt off as quickly as possible is always the most cost-effective strategy.

Understanding Federal Tax Liens

If you owe a significant amount of tax, the IRS may file a Notice of Federal Tax Lien. This is a public legal claim against your property, securing the government's interest in your assets. A tax lien can harm your credit and make it difficult to sell property. However, setting up a Direct Debit Installment Agreement can sometimes lead to a withdrawal of a filed Notice of Federal Tax Lien, offering a path to clear your public record.

Importance of Future Tax Compliance

Once you have an agreement in place, you must remain compliant with all future tax laws. This means filing all future tax returns on time and paying any new taxes owed in full. Failure to do so will cause your existing agreement to default, potentially leading to immediate and aggressive collection actions.

Managing and Monitoring Your Payment Plan

Use your IRS online account to manage your plan. You can view your payment history, see your remaining balance, and even revise your payment amounts or due dates in some cases. Staying on top of your agreement is key to successfully resolving your debt.

When to Seek Professional Tax Help

If your tax debt is substantial, if you have multiple unfiled returns, if you are facing a federal tax lien, or if you simply feel overwhelmed by the process, it is wise to consult a qualified tax professional. They can navigate the complexities of IRS procedures, negotiate on your behalf, and help you find the best possible resolution.

Conclusion: Don't Give Up – Solutions Are Available

Receiving a "not eligible" message from the IRS online payment system is a common hurdle, not a final roadblock. It is an indication that your situation requires a more personalized approach. By understanding the reasons for the denial, gathering your financial information, and proactively exploring the full range of payment plan options—from a short-term payment plan to a non-streamlined installment agreement—you can take back control. The key is to act promptly and deliberately. The Internal Revenue Service provides multiple pathways to resolve tax debt, and a solution is almost always within reach.