IRS Form 8300 Guide: Reporting Cash & Avoiding Penalties

Discover everything you need to know about IRS Form 8300 with our comprehensive guide. Learn how to report cash payments over $10,000 and avoid penalties.

Elaine Carter

9/16/20259 min read

IRS Form 8300 for Businesses: A Complete Guide to Reporting $10,000+ Cash & Avoiding Penalties

If your business accepts large cash payments, a single transaction over $10,000 could trigger a crucial reporting requirement to the federal government. This isn't just a matter of bookkeeping; it's a legal obligation with significant consequences. The tool at the center of this requirement is IRS Form 8300, a document that places your business on the front lines in the fight against financial crime. Failing to understand and comply with these rules can lead to severe civil and criminal penalties, putting your hard-earned reputation and financial stability at risk.

Understanding the Purpose of Form 8300

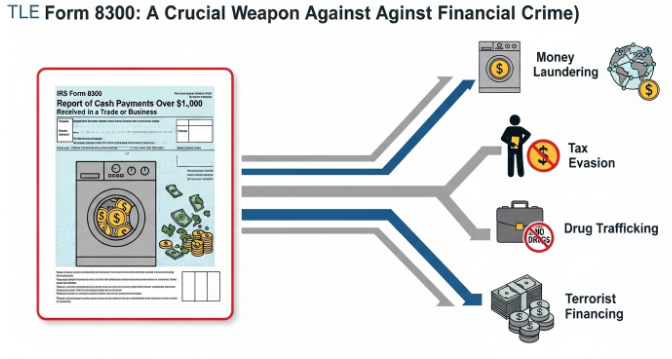

IRS Form 8300, Report of Cash Payments Over $10,000 Received in a Trade or Business, is a joint document used by the Internal Revenue Service (IRS) and the Financial Crimes Enforcement Network (FinCEN). Its primary purpose is to create a paper trail for large cash transactions. This information is a vital resource for law enforcement agencies tracking illicit funds moving through legitimate businesses. By reporting these payments, you provide valuable data that helps uncover criminal activities.

The Importance of Compliance: Combating Money Laundering and Tax Evasion

How Form 8300 Helps Combat Financial Crime

The legal foundation for Form 8300 lies within the Bank Secrecy Act and Title 26 of the U.S. Code. This legislation aims to prevent financial institutions and businesses from being used as tools for illegal enterprises. Every filed Form 8300 contributes to a national database used to identify and prosecute individuals involved in money laundering, tax evasion, drug trafficking, and terrorist financing. The scale of this issue is immense; in 2025 alone, an estimated USD 300 billion in money is laundered in the USA. Compliance is not just a regulatory hurdle; it's a business's contribution to national security and economic integrity.

Who This Guide Is For: Businesses Receiving Large Cash Payments

This guide is for any individual or entity operating a "trade or business" that receives more than $10,000 in cash. This includes, but is not limited to, sole proprietorships, partnerships, corporations, and LLCs. Whether you sell high-value goods like cars or jewelry, provide professional services, or deal in real estate, understanding your Form 8300 obligations is non-negotiable if you handle large cash payments.

The Promise: A Complete Guide to Reporting and Penalty Avoidance

Navigating IRS regulations can be complex, but this guide will demystify Form 8300. We will break down what constitutes a reportable cash transaction, explain the critical concept of related transactions, detail who must file, and walk you through the filing process. By the end, you will have a clear, actionable roadmap for compliance, helping you avoid costly penalties and protect your business.

What Constitutes a Reportable Cash Transaction?

The trigger for filing Form 8300 is receiving more than $10,000 in "cash" in a single transaction or in related transactions. The first step to compliance is understanding precisely what the IRS considers to be a reportable event.

Defining "Cash" for Form 8300

The definition of "cash" for Form 8300 purposes is broader than just physical bills and coins. It includes:

U.S. and Foreign Currency: The most straightforward form of cash. The value of any foreign currency must be converted to U.S. dollars to determine if the threshold is met.

Cashier's Checks, Money Orders, Bank Drafts, and Traveler's Checks: These instruments are treated as cash if they have a face value of $10,000 or less and are used in a transaction where the total cash and cash-equivalents received exceed $10,000. This rule is designed to prevent individuals from structuring payments to avoid reporting.

The $10,000 Threshold: Simple Breakdown

The rule is clear: if you receive Cash Payments Over $10,000, a report is required. This applies whether the payment is for goods, services, real estate, intangible property, or debt repayment. If a customer walks in and pays you $12,000 in currency for a product, you must file Form 8300. The reporting obligation is triggered the moment the total reportable cash received crosses that threshold.

What Does NOT Count as Cash

It is equally important to know what is not considered cash. Personal checks, regardless of the amount, are not cash for Form 8300 purposes. The same applies to payments made via wire transfer, ACH, or credit/debit card, as these transactions already have an electronic trail through the financial system.

The Critical Concept of "Related Transactions"

One of the most complex areas of Form 8300 compliance is the rule regarding related transactions. Criminals often attempt to evade reporting by breaking down a large cash payment into smaller amounts, a practice known as "structuring." The related transaction rule is designed to counteract this tactic.

Aggregating Multiple Payments to Reach the $10,000 Threshold

A business must file Form 8300 if it receives multiple cash payments that are part of a single transaction or a series of related transactions, and the total of these payments exceeds $10,000. If a customer makes a $6,000 cash down payment on a car one week and pays the remaining $5,000 balance in cash the following week, the two payments must be aggregated. Because the total of $11,000 exceeds the threshold, a Form 8300 is required.

The 12-Month Lookback Rule

The aggregation rule extends over time. A business must file Form 8300 when the total cash received from a series of related transactions exceeds $10,000 within a 12-month period. The filing deadline is 15 days after receiving the payment that pushes the cumulative total over the $10,000 mark. If you receive an initial payment that is under the threshold, you must keep track of it. When a subsequent related payment brings the total over $10,000, the reporting requirement is triggered.

Practical Examples of Related Transactions

Retail: A customer buys a $12,000 watch and pays for it with three separate cash payments of $4,000 over three consecutive days. These are related transactions, and a Form 8300 must be filed.

Contracting: A homeowner pays a contractor $15,000 for a renovation project in three cash installments of $5,000 over two months. These are related, and the contractor must file.

Legal Services: A client pays a law firm a $5,000 cash retainer and later pays an additional $6,000 in cash for services on the same case. The firm must report the transaction.

Identifying and Tracking Related Transactions Effectively

To comply, businesses must implement a robust tracking system. When a customer makes a cash payment, staff should check if that customer has made other recent cash payments. This can be managed through your point-of-sale system, customer relationship management (CRM) software, or even a dedicated manual log. The key is to have a consistent process for identifying and aggregating payments from the same customer for the same or related purposes.

Who Is Required to File Form 8300?

The filing requirement applies to any "person" engaged in a "trade or business" who receives a qualifying payment. The IRS defines these terms broadly to ensure wide coverage.

Businesses Engaged in a "Trade or Business"

A "trade or business" is any activity carried on for the production of income from selling goods or performing services. This encompasses nearly all for-profit ventures, from large corporations to self-employed individuals. If you operate a business, the Form 8300 rules apply to you.

The "Recipient" of Cash: Who Has the Filing Obligation

The obligation to file rests with the person or business that receives the cash. It is not the payer's responsibility. If an employee accepts a qualifying cash payment on behalf of the business, the business itself is the recipient and must file the form. The business's name, address, and Employer Identification Number (EIN) must be included.

Geographic Scope: U.S. Territories and Jurisdictions (e.g., Puerto Rico, American Samoa, Washington, DC)

The Form 8300 filing requirement is not limited to the 50 states. It applies to all businesses operating within the United States and its territories and possessions. This includes Puerto Rico, the U.S. Virgin Islands, Guam, American Samoa, and the Northern Mariana Islands. Businesses in Washington, DC, are also subject to the same rules.

When Charitable Organizations or Exempt Entities Must File

Even tax-exempt organizations, such as charities, may be required to file Form 8300. While genuine charitable donations are not reportable, if an exempt organization is engaged in a trade or business activity unrelated to its tax-exempt purpose (e.g., selling merchandise in a gift shop or renting out property), it must report cash payments over $10,000 received from those activities.

When and How to File Form 8300

Timely and correct filing is essential to avoid penalties. The process involves a strict deadline and specific submission methods.

The 15-Day Filing Deadline: Understanding the Clock

You must file Form 8300 within 15 days of the date you receive the cash. The clock starts the day after the transaction. If the 15th day falls on a Saturday, Sunday, or legal holiday, you have until the next business day to file. For related transactions, the 15-day window begins on the day the cumulative amount of cash received exceeds $10,000.

Methods of Filing

There are two ways to file Form 8300: electronically or by mail.

Electronic Filing: The IRS encourages electronic filing through FinCEN's Bank Secrecy Act (BSA) E-Filing System. It is free, secure, and provides an instant confirmation of receipt. As of 2024, businesses required to e-file certain other information returns (like Forms 1099) must also e-file their Forms 8300.

Paper Filing: If you are not required to file electronically, you can mail the form to the IRS processing center at the Detroit Federal Building.

Completing Form 8300: A Section-by-Section Guide

Accuracy is paramount when completing Form 8300. The form is divided into four main parts, each requiring specific information about the transaction and the parties involved.

Part I: Identity of Individual From Whom Cash Was Received

This section captures information about the person who physically brought the cash to you. You must include their full name, address, date of birth, and occupation. Crucially, you must request their Taxpayer Identification Number (TIN), which is typically a Social Security Number (SSN). You are also required to verify their identity using a government-issued document, such as a driver's license or passport, and record the document details on the form.

Part II: Person on Whose Behalf This Transaction Was Conducted

This part is only completed if the person in Part I was conducting the transaction for someone else. For example, if an agent makes a cash payment on behalf of their client, you would enter the agent's information in Part I and the client's information in Part II. This ensures that law enforcement can identify the true source of the funds.

Part III: Description of Transaction and Method of Payment

Here, you describe the nature of the transaction. Specify what was sold or the service rendered. You must detail the total cash amount received, breaking it down by the amount in $100 bills and the amount in other currency or cash equivalents. If the transaction appears suspicious (e.g., the customer seems intentionally evasive), there is a box to check to flag it as a suspicious transaction.

Part IV: Business That Received Cash

This final section is for your business's information. You must enter your business name, address, Employer Identification Number (EIN) or SSN if you're a sole proprietor, and the nature of your business. This part is signed by an authorized individual, certifying that the information is true and correct.

Common Mistakes and How to Avoid Them During Completion

Common errors include leaving fields blank, especially the TIN, failing to verify the payer's identity, or providing a vague description of the transaction. To avoid these mistakes, establish a clear procedure for collecting all required information at the time of the transaction. Politely explain to the customer that this is a federal requirement and that you need their full cooperation. Never leave the TIN field blank; if the customer refuses to provide it, you must note this on the form.

Conclusion

Compliance with IRS Form 8300 is a fundamental responsibility for any business that deals in large cash transactions. It is more than a bureaucratic task; it is a vital mechanism that protects your business from being implicated in financial crimes like money laundering and provides law enforcement with crucial intelligence. Failing to file correctly can result in substantial penalties; for instance, in 2023, penalties for failure to file could reach $290 per occurrence. Willful non-compliance can escalate to a criminal offense with even more severe criminal sanctions.

To ensure compliance and safeguard your business, follow these key steps:

Understand the Definitions: Know exactly what the IRS considers "cash" and a "reportable transaction."

Track Relentlessly: Implement a system to identify and aggregate related transactions to ensure you catch payments that cross the $10,000 threshold over time.

File Promptly and Accurately: Adhere to the 15-day deadline and embrace electronic filing for efficiency and confirmation. Collect all required customer information, including their Taxpayer Identification Number, at the time of sale.

Notify Your Customer: Remember to provide a written statement to the customer by January 31 of the year following the transaction, informing them that you have filed a Form 8300.

Keep Records: Retain copies of all filed Forms 8300 and related customer notification statements for at least five years.

By treating Form 8300 not as a burden but as an integral part of your business's risk management and civic duty, you can operate with confidence, avoid severe penalties, and maintain a reputation of integrity in the marketplace. If you encounter complex scenarios or have any doubts, consulting with a tax professional is always a prudent investment.