IRS CP2000 Notice Guide: Understand & Respond Effectively

Received an IRS CP2000 notice? Discover how to understand and respond to underreported income issues with our comprehensive guide.

Elaine Carter

9/16/20257 min read

IRS CP2000 Notice: Your Essential Guide to Understanding and Responding to Underreported Income

The arrival of a letter from the Internal Revenue Service can trigger immediate anxiety. When that letter is an IRS CP2000 Notice, it’s easy to assume the worst. This notice, however, is not a formal audit, but rather a proposal from the IRS suggesting a change to your tax return based on a discrepancy. The Internal Revenue Service (IRS) automated systems compare the income you reported on your individual income tax return with information provided by third parties, such as employers and financial institutions. When a mismatch occurs, a CP2000 is generated. While the IRS conducted 505,514 audits in fiscal year 2024, a CP2000 notice is part of a separate, automated process. Understanding what this tax notice means and how to respond correctly is the first step toward resolving the issue efficiently and calmly.

Introduction: Navigating the Unexpected IRS CP2000 Notice

Don't Panic: Acknowledge the initial stress of receiving an IRS CP2000 notice.

Receiving any official correspondence from the IRS can be unsettling. A CP2000 notice, with its proposed tax increase and detailed calculations, often looks intimidating. It’s crucial to remember that this notice is a common, automated inquiry, not an accusation of wrongdoing. Your initial reaction of stress is normal, but it shouldn't lead to inaction.

The Core Message: While a CP2000 can be daunting, it's manageable with the right information and action.

The key to handling a CP2000 notice is a methodical and timely response. This is a solvable problem. Whether you agree with the IRS, disagree entirely, or find yourself somewhere in between, there is a clear process to follow. With the right approach, you can navigate the notice, protect your rights, and achieve a fair resolution.

Understanding Your IRS CP2000 Notice: What It Is and Why You Received It

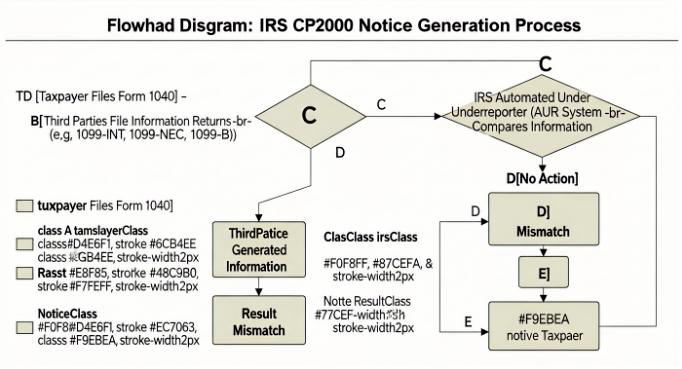

How an IRS CP2000 Notice Is Generated

Defining the CP2000 Notice: Not an Audit, But a Proposed Adjustment

An IRS CP2000 is fundamentally a proposal, not a final bill or an audit. The IRS believes there is a discrepancy between the income and/or payment information reported by third parties and the amounts you reported on your tax returns. This notice outlines the proposed changes, calculates the potential additional tax, and includes any applicable penalties and interest. It is your opportunity to review, agree, or contest the findings before the IRS makes a final determination.

The Root Cause: Income Mismatch and Information Returns

The IRS CP2000 process is driven by data matching. The agency's Automated Underreporter (AUR) system compares your Form 1040 with millions of information returns filed under your Social Security Number. These information returns include forms like the Form 1099-INT from your bank, a Form 1099-B from your brokerage, or a Form 1099-NEC from a client. If you forgot to report interest income or misreported the cost basis on a stock sale, the AUR system will flag the mismatch and generate one of these CP2000 notices.

Key Elements of Your CP2000 Notice: What to Look For

When you receive your CP2000, locate these key items. You will find the Notice Number and date in the top right corner. The body of the letter will detail the specific income or payment items in question, showing what you reported versus what the IRS has on file. Most importantly, it will present a summary of the proposed changes, including the calculated tax increase, penalties, and interest, culminating in a proposed balance due.

Your Immediate Steps: Evaluating the CP2000 Notice with a Strategic Mindset

Step 1: Breathe and Gather Your Records

Before you do anything else, take a moment to pause. Do not rush to pay a balance you haven't verified. Instead, collect all relevant tax documents for the year in question. This includes your original tax return, all W-2s, and every Form 1099 you received for income, investments, or other financial activities. Having these documents on hand is essential for the next step.

Step 2: Compare and Verify the IRS's Information

Carefully compare the information detailed in the CP2000 notice with your own records. Did you forget to include a Form 1099 from a freelance gig? Is the IRS proposing a change based on a duplicate information return filed by a payer? Did you correctly report the cost basis for a stock sale listed on Form 1099-B? Sometimes the IRS is correct; other times, their information is incomplete or wrong.

Step 3: Understand Your Rights and the Consequences of Inaction

You have the right to agree or disagree with the proposed changes. You also have a specific deadline to respond, typically 30 days from the date on the notice. Ignoring a CP2000 is the worst course of action. Failing to respond will lead the IRS to assume you agree with their proposed tax increase. They will then issue a formal Statutory Notice of Deficiency, which gives you 90 days to either pay the balance or petition the U.S. Tax Court before they begin collection actions.

Responding to Your CP2000 Notice: A Strategic Action Plan

Option 1: You Agree with the IRS's Proposed Changes

If your review confirms the IRS is correct and you underreported income, the simplest path is to agree. You will sign the enclosed Response form, indicating your agreement, and return it by the deadline. If you can pay the full balance due, include a check with the response voucher. If you cannot afford the full amount, you should still return the form and explore payment options like an installment agreement or a short-term payment plan.

Option 2: You Disagree (Fully or Partially) with the IRS's Proposed Changes

If you find that the IRS's information is incorrect or incomplete, you must formally disagree. Check the "I do not agree" box on the Response form. Your CP2000 response must include a signed statement explaining precisely why you disagree and provide copies of supporting documentation. This could include corrected Form 1099s, bank statements, or brokerage records proving your position. It is critical not to file an amended return (Form 1040-X) unless specifically instructed to do so by the IRS, as this can complicate the resolution process.

Option 3: You Need More Time or Clarification

If you cannot gather your documents or formulate a response by the deadline, you can call the phone number on the notice to request an extension. The IRS is often willing to grant a 30-day extension. This is far better than sending an incomplete response or no response at all. Use this time to organize your records or consult with a tax professional.

Navigating Deeper Disagreements: The Appeals Process and Beyond

When the IRS Still Disagrees: Receiving a Statutory Notice of Deficiency

If you respond with a disagreement but the IRS rejects your explanation, they will issue a Statutory Notice of Deficiency (also known as a 90-day letter). This is a legally significant document that formalizes the IRS's determination. It starts a 90-day clock during which you must either agree to the assessment or file a petition with the U.S. Tax Court.

The IRS Office of Appeals: Your Right to a Fair Review

Before heading to court, you have the right to request a conference with the IRS Office of Appeals. This is an independent division within the IRS tasked with resolving tax disputes without litigation. An Appeals Officer will review the case from both sides—yours and the examiner's—to see if a settlement can be reached. This is often an effective venue for resolving complex disagreements.

Considering Tax Court: Your Last Resort for Disputing

If you and the Office of Appeals cannot reach an agreement, your final option is to petition the U.S. Tax Court within the 90-day window. This is a formal legal proceeding where a judge will hear your case and make a final ruling on the tax liability. Litigating in Tax Court is a serious step and almost always requires the expertise of a qualified tax attorney.

Preventing Future CP2000 Notices: Proactive Strategies for Accuracy

Mastering Your Information Returns: Reconciliation is Key

The most effective way to avoid a CP2000 notice is to meticulously reconcile all information returns with the income reported on your tax return. Before filing, create a checklist of all expected Form 1099s and W-2s. As they arrive, check them off and ensure the figures are entered correctly. With over 271.5 million tax returns filed in 2023, automated matching is the IRS's primary tool for finding errors.

Diligent Record-Keeping: A Foundation for Accurate Reporting

Maintain organized records throughout the year, not just at tax time. This includes tracking all income sources, especially for freelance or gig work, and keeping detailed records of investment transactions, including purchase dates and cost basis. Good records not only ensure accurate filing but also provide the necessary proof should you ever need to dispute an IRS notice.

The Value of Professional Tax Preparation

Using reputable tax software or hiring a tax professional can significantly reduce the risk of errors that trigger a CP2000. These professionals are familiar with common reporting pitfalls and can help ensure all income is correctly accounted for, from simple interest to complex transactions reported on forms like Form 1099-B or educational credits on Form 8863.

When to Seek Expert Help: Your Tax Professional as an Ally

Signs You Need Professional Assistance:

While you can handle a simple CP2000 on your own, you should seek help if the notice involves a large proposed tax increase, complex issues like investment basis or business income, or if you disagree with the IRS and aren't confident in your ability to present your case. The projected gross tax gap for 2022 is $696 billion, a figure that underscores the IRS's motivation to ensure compliance, making a strong response crucial.

Choosing the Right Tax Professional: What to Look For

Look for a credentialed professional with experience handling IRS notices, such as an Enrolled Agent (EA), a Certified Public Accountant (CPA), or a tax attorney. These individuals can represent you before the IRS, communicate directly with the agency on your behalf, and help you navigate the appeals process if necessary. They can analyze the notice, craft a strategic CP2000 response, and work toward the best possible outcome.

Conclusion: Respond Strategically, Prevent Proactively

An IRS CP2000 notice is a manageable issue when approached with a clear strategy. The key is to remain calm, act promptly, and respond thoughtfully. By understanding the nature of the notice, carefully evaluating the IRS's claims against your own records, and knowing your response options, you can take control of the situation. Whether you agree, disagree, or need help from a professional, your response is the critical factor in determining the outcome. By implementing proactive measures like diligent record-keeping and thorough income reconciliation in the future, you can significantly reduce the chances of receiving another one.

Key Takeaways: Don't ignore the CP2000 notice, understand its nature, and respond strategically.

Your primary takeaways should be to never ignore an IRS notice, to recognize that a CP2000 is an automated proposal and not a formal audit, and to choose your response method—agree, disagree, or request more time—based on a careful review of the facts. If the situation feels overwhelming, engaging a tax professional is a wise investment in securing a proper and fair resolution.